Mezo Earn: A ve(3,3) System for Bitcoin Lending

Mezo Earn is a Bitcoin-native lending and vote-escrow system where users lock BTC, earn BTC-denominated yield, and direct incentives across lending, DEX liquidity, and vaults. Learn how veBTC, veMEZO, gauge voting, and Bitcoin-backed liquidity work together.

If you've locked AERO and voted on gauges, you'll recognize much of what Mezo is building. On Aerodrome, you are coordinating liquidity for a DEX. On Mezo, you're coordinating an entire Bitcoin economy.

Mezo’s vote-escrow system is built specifically for a Bitcoin-native economy, where BTC remains the base asset, governance anchor, and primary source of value accrual.

Specifically, Mezo’s vote-escrow weight is divided across two tokens, with locked BTC providing the base voting power, and locked MEZO boosting voting power up to 5x. Votes direct capital across a lending market, a DEX, and automated vault strategies, rather than only liquidity pools.

The ve Model You Already Know, Built for Bitcoin

Curve started the idea. Solidly tried to finish it. Aerodrome proved it works.

On Aerodrome, users lock AERO, receive veAERO, vote on pools, and earn fees and bribes. Pools with the most votes receive the most emissions, which attract more liquidity and generate more fees. The flywheel spins because every participant has a lever that matters.

Mezo applies that same coordination model to Bitcoin.

The Dual-Token System

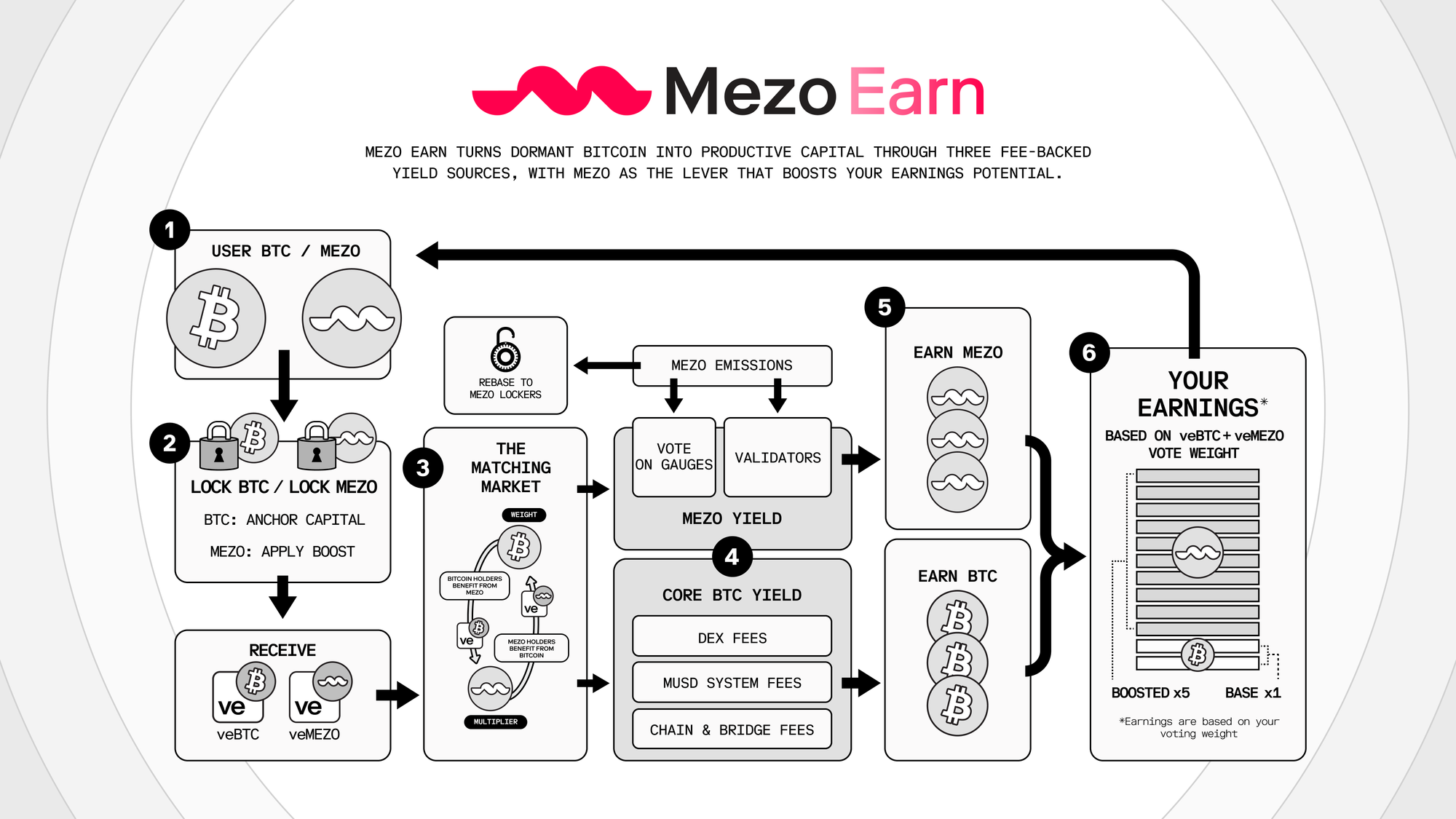

Mezo is a decentralized Bitcoin lending platform. Users lock BTC as collateral, borrow MUSD (a Bitcoin-backed stablecoin) against it, and access dollar liquidity without selling their BTC. Borrowing, trading, and bridging activities all generate BTC-denominated fees that flow back to participants.

Mezo’s ve-system determines who captures those fees and where additional incentives are directed. On Aerodrome, veAERO handles both functions in a single token. On Mezo, those functions are split into two.

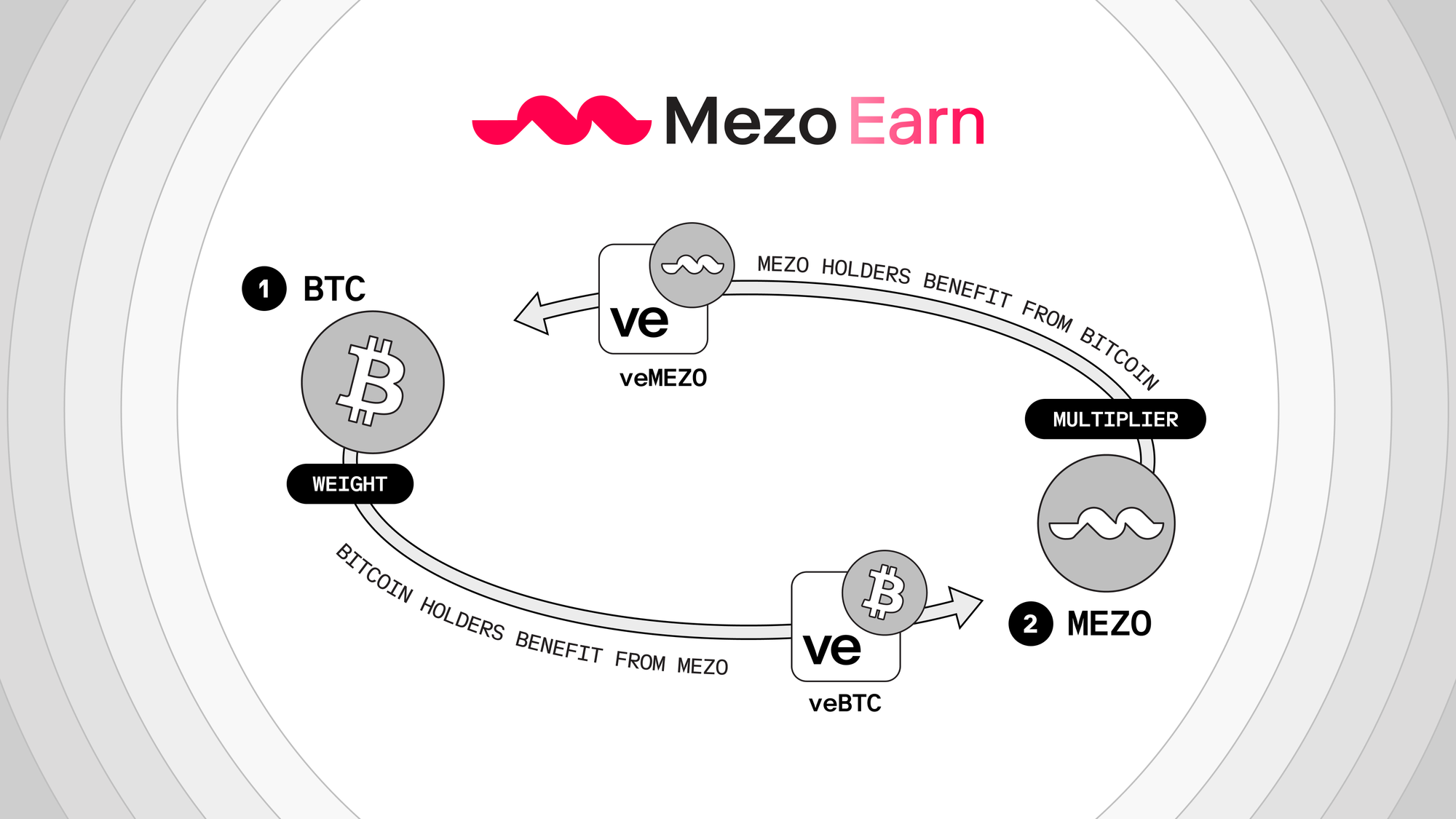

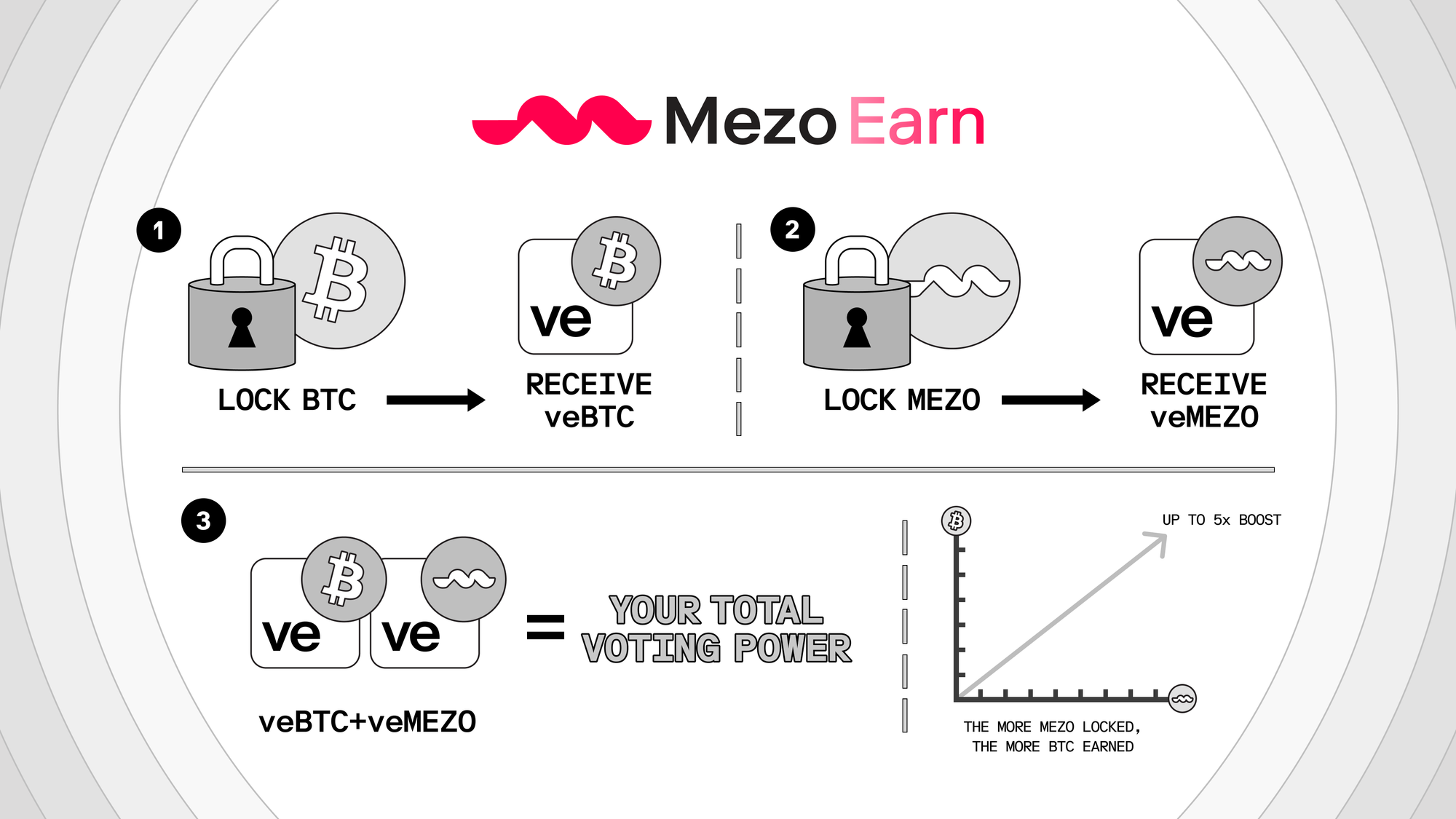

→ veBTC is the base asset. Lock BTC, receive veBTC. This is your base voting asset. veBTC earns a base BTC-denominated fee passively from all chain activity. It also gives you voting power to direct where additional fees and emissions flow. Locks are short by design, with a maximum of 30 days. You never need anything other than BTC to participate and earn.

→ veMEZO is the booster asset. Lock MEZO, receive veMEZO. veMEZO increases the effective weight (aka boosts) of a veBTC position up to 5x, meaning a larger share of the fee distribution. The longer you lock, the more voting power you get. However, veMEZO can be productive on its own. veMEZO holders can direct their votes to any veBTC gauge and collect the incentives that BTC holders post.

How veBTC and veMEZO combine

Every veBTC position starts at a 1x multiplier. Lock BTC, receive base voting weight, earn a share of bridging and chain fees. No MEZO required.

This is the base case. veMEZO scales that voting power up to 5x.

The boost depends on a user's relative share of the total veBTC pool and relative share of the total veMEZO pool. When your share of veMEZO is proportionally as large as your share of veBTC, you reach the cap.

Two properties define this mechanism:

- The cap is hard. No combination of BTC and MEZO produces a multiplier above 5x. The system rewards proportional commitment, not accumulation.

- The boost scales inversely with BTC position size. A large BTC holder needs a proportionally larger share of veMEZO to reach the same multiplier a smaller holder achieves with less. Large positions cannot dominate governance without proportional MEZO commitment.

In simpler terms: if you own 10% of all veBTC, you need 10% of all veMEZO to hit max boost. A participant with 1% of veBTC only needs 1% of veMEZO. The formula enforces parity.

The Matching Market

On Aerodrome, gauges attach to pools. Protocols post bribes, veAERO holders direct emissions, and the market exists between protocols and voters. Mezo's system is also built for a secondary market, where gauges can be attached to individual BTC positions. Now, the relationship between BTC holders and MEZO holders has become a market in its own right.

Every veBTC NFT receives its own gauge. veMEZO holders vote on these gauges. The more veMEZO weight directed at a specific veBTC gauge, the higher that position's boost.

This creates a two-sided market:

→ BTC-heavy, MEZO-light: Post incentives on your veBTC gauge to attract veMEZO votes. Boost becomes something you pay for rather than something you must self-optimize into.

→ MEZO-heavy, BTC-light: Survey the available veBTC gauges, find those with the best incentive yield, allocate veMEZO votes accordingly. MEZO converts into a claim on BTC-derived fee flows without requiring proportional BTC exposure.

Boost becomes a permissionless, tradeable service.

If you're an Aerodrome voter, the logic is familiar. Just like you compare Aerodrome pools by bribes per vote, on Mezo, you can compare veBTC gauges by incentive yield per veMEZO vote. Same instinct, different market.

Where You Vote

On Aerodrome, every liquidity pool has a gauge. Mezo uses a similar gauge concept, but the surface area is wider. There are five places your vote has an impact on:

- DEX liquidity pools. BTC/MUSD pairs and other trading pools and pairs on Mezo's native DEX. Any pool on the Mezo DEX can have a gauge. Directing emissions to a pool can deepen trading liquidity and generate swap fees.

- The MUSD Savings Rate. A gauge that directs value toward MUSD savers. Think of it as voting to improve the yield for people holding MUSD in the savings vault.

- Individual veBTC positions. This is where Mezo differs from Aerodrome. Every locked BTC position gets its own personal gauge. veMEZO holders vote on these individual gauges to boost specific veBTC positions. veBTC holders can post incentives on their gauge to attract your votes. This is the matching market described above.

- Validators. Emissions can flow to validators securing the network.

- Ecosystem programs. Grants, development, and growth initiatives.

A governed splitter system determines how emissions are divided across these categories each epoch. The ratios shift gradually, a maximum 1% per epoch, preventing abrupt reallocations and keeping the system predictable.

What Makes This Different

Aerodrome is built around the idea that AERO should sit at the center of the system. You lock AERO, you vote with AERO, emissions are denominated in AERO, and the entire coordination game revolves around AERO. That makes sense for a DEX. The protocol’s job is to allocate liquidity incentives, and the protocol token is the natural unit of coordination.

Bitcoin is different. BTC is not a governance token, and trying to force it into that role usually breaks the thing that makes Bitcoin valuable in the first place. People hold BTC because it is often viewed as a reserve asset. They do not hold it because they want exposure to a protocol’s inflation schedule, political process, or reflexive token game. In a Bitcoin-native system, Bitcoin should be king.

Mezo's design respects that. veBTC carries base voting weight and earns fees. veMEZO multiplies that weight, up to 5x, but has no independent governance power on its own. A veBTC position with zero veMEZO votes still works at 1x. It still earns BTC-denominated bridging and chain fees passively, without voting. You never need MEZO to participate (though holding veMEZO to increase your vote weight may be advantageous). MEZO's sole purpose is to coordinate around BTC.

That sounds subtle, but it changes the market structure completely.

On Aerodrome, protocols bribe veAERO voters to direct emissions to their pools. The relationship is between protocols and voters. On Mezo, every veBTC position gets its own gauge. BTC holders who want higher multipliers can post incentives on their gauge to attract veMEZO votes. MEZO holders may scan across all veBTC gauges and vote wherever the yield per veMEZO is highest. It's a two-sided matching market between individual BTC holders and individual MEZO holders.

Rebases work differently as well. Aerodrome mints rebases on top of scheduled emissions. More locking means more total inflation. Mezo allocates rebases from within the fixed weekly emission budget. The rebase share is a function of how much MEZO is unlocked, squared. When locking is low, up to half of weekly emissions go to rebases, which may pull MEZO into locks. As locking increases, that share drops fast, and more emissions flow to gauges and validators. Total supply growth stays on schedule regardless of lock behavior.

And finally, but most importantly, Mezo passes the test that most Bitcoin products fail: yield is paid in BTC. That revenue comes from MUSD loan interest, DEX swap fees, and bridging and chain fees. Fees flow passively to all veBTC holders by weight. Swap fees and MUSD revenue can be diverted from stakers to veBTC voters through gauges, the same pattern Aerodrome uses for trading fees. The difference is that the base layer of yield (bridging fees) requires no active management. You lock BTC, you earn BTC.

Start Earning Today

Lock BTC and start voting at mezo.org/earn. Epochs run weekly (Thursday to Thursday), and your first vote qualifies you for fee distribution that same epoch. Track TVL, lock rates, gauge weights, and fee generation onchain at dune.com/mezo/proof-of-hodl.

Follow @MezoNetwork for weekly epoch recaps and protocol updates.

For the full technical breakdown of the dual-token mechanics, boost formula, splitter hierarchy, and anti-dilution math, read The Mezo Earn Whitepaper.

To learn more:

- The Mezo Earn Whitepaper

- Introducing MEZO

- Introducing Mezo Earn

- Where Does the Yield Come From?

- Mezo on X

- Mezo Discord

This material contains forward-looking statements regarding future events, milestones, development, and utility. Such statements are based on current expectations and assumptions and are subject to risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied. Digital assets are highly volatile assets with no guaranteed value, utility, or performance. Participation involves significant risk, including but not limited to price volatility, regulatory uncertainty, technological vulnerabilities, and liquidity risk. Participation may result in partial or total loss of funds. The materials do not constitute, and should not be construed as, financial, investment, or legal advice. Participants must conduct their own due diligence on all relevant matters, and seek advice from legal, tax, or financial advisors regarding the risks and consequences of participation. All actions taken are done so at your own risk.